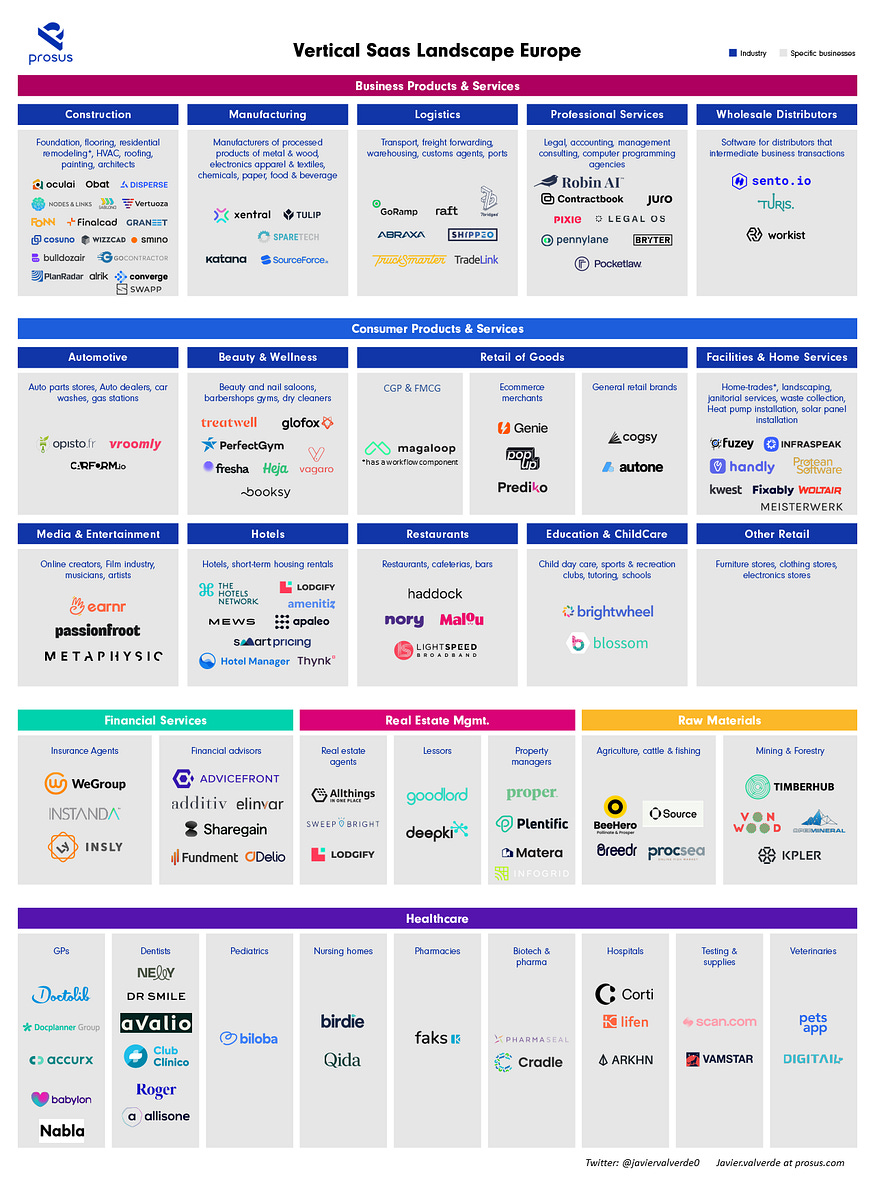

Vertical Software (and AI)

(2023 view, 1 year delayed posting)

Over the past decade, we have seen the increasing success of software solutions focused on specific industries, Veeva (pharma), ServiceTitan (home services), Procore (construction), Toast (restaurants) and Mindbody (gyms).

Industry-specific software, ‘Vertical SaaS’, has a lot of opportunities going forward, and new AI advancements are an accelerant on this stack (‘Vertical AI’). In this article I attempt to provide a framework for prioritizing what industries to pursue, what architectural decisions to make, and how AI may evolve vertical SaaS from a system of record to a system of action.

What elements can make an attractive industry for building a large vertical SaaS business?

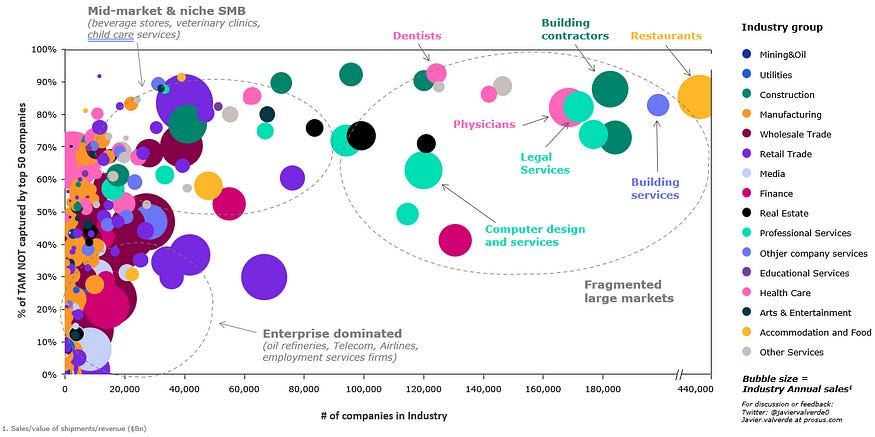

But first, for those building in the space, what elements can make a good industry for building a large vertical SaaS business? While each industry potential should be evaluated independently, the most generalizable factors are: 1). Large end-markets. E.g. there are 124,000 dentist companies in the US, making $126bn in revenue annually and 2). Some level of fragmentation. E.g. top 50 dentist companies only make up 7% of total industry sales, meaning most of the market is not controlled by a set of large companies.

Based on the US census, we analyzed the size and fragmentation of over 1,000 industries to identify potentially fertile spaces for vertical SaaS to flourish. Industries that are large and fragmented.

Successful companies can be built in any of the above three dotted circles, but there are common pitfalls to watch for in each:

Fragmented large markets ‘goldilocks?’ (top right) includes industries like restaurants, building contractors, or law firms.

Upside: Industries that are both large in customers and fragmented in concentration create pricing power with a large TAM

Downside: Due to its more attractive structure, some of its verticals may find more competition from startups or incumbents. For instance, the restaurant segment has strong incumbents like Toast, and the home services segment has ServiceTitan. In addition, very fragmented industries can have SMBs with low annual contract values, which may need an adapted go-to-market.

The possible opportunity: Companies may find opportunities here through regional-specific plays (e.g. building the Toast for Middle East) or by further specializing within a vertical (e.g. Roofr specialized within a subsegment of construction contractors: roofing contractors).

The more specialized market ‘Happy Medium’ (top left) includes industries like auto dealers, machinery wholesalers, or veterinaries.

Upside: These categories of SaaS tend to have lower competition historically, so the software being displaced can be antiquated or not purpose-built for the industry. Therefore, the bar to add value can be lower.

Downside: A possibility of small TAMs. It’s important to ensure that the SaaS and expansion opportunities allow for the building of a large enough business. In this bucket, the ‘layer cake’ approach can be more important.

The possible opportunity: The new infrastructure in fintech can lead to more monetization, while AI allows for software creation with less resources and higher workflow automation. This may enable SaaS companies to capture more value earlier on (a higher take rate on industry size), and may make smaller verticals attractive for venture investment.

The large customer-dominated ‘Enterprise District’ (bottom left) includes industries like oil refineries or telecoms.

Upside: Larger customers can lead to bigger contracts and also tend to have higher retention than smaller ones.

Downside: Given the size of larger customers, there can be longer sales cycles. Additionally, an aversion from larger companies to work with startups can pose a challenge to growth.

The possible opportunity: The opportunity with large enterprise-dominated sectors may require a different approach. Large enterprises often already have a System of Record (SOR — see below for more detail), for many it is their ERP system. As such, the opportunity may lie in building specific high-value workflows on top of the existing system of record.

At a business level, what elements can make good architectural product decisions?

The best vertical SaaS companies are a system of record for important company data, paired with operational workflows and the opportunity to build an ecosystem of new offerings on top. There are five general attributes that can help create a larger vertical SaaS business.

1) A System of Record. This is the source of truth for important company data — a vital database where the key is a foundational data unit for a major part of the business. A business typically only has one or a few critical data keys — this may be the customer unit, the supplier unit, the inventory, the shipment, the construction project, etc. Now with Large Language models to interpret data, the key data may be customer calls embedded in a database. On top of this business-critical data, a SaaS can have stronger retention and build workflows.

2) A ‘layer cake’ of offerings on top of the core system of record and workflows. Some examples are SaaS multiproduct, B2C payments, procurement / B2B marketplace, working capital finance, B2C e-commerce (with the SaaS customer as the traffic driver), insurance distribution, consulting services, payroll management, etc.

3) Target a level of gross margin per customer that allows for a 12-month payback at a gross margin level. For larger and higher retention customers, payback periods could be longer. Joe at a16z makes a case here for why typically gross margin per customer per year should be over $5–10k if a sales motion is needed to scale. There are examples of vertical SaaS companies that make exceptions to this guideline: Mindbody’s gross margin per customer was $1,000 when Bessemer invested in 2010. The company was able to grow from $10M to $180M in revenues in the next 7 years (gross margin per customer was still only ~$2,000 per customer in 2017).

4) Find a wedge to make the sales process and onboarding easier and faster. We saw a top vertical SaaS founder build free data tools for customers in partnership with the industries’ association to overcome the customer’s key risk — loss of data and downtime on the transfer between software products.

5) An early team member with previous industry background. This can shape initial insight and establish contacts, making the journey easier. Nevertheless, we have seen great founders learn the industry not far before founding the company and, over time, gain a deep understanding of the problem’s significance.

How generative AI could create a new opportunity in vertical SaaS

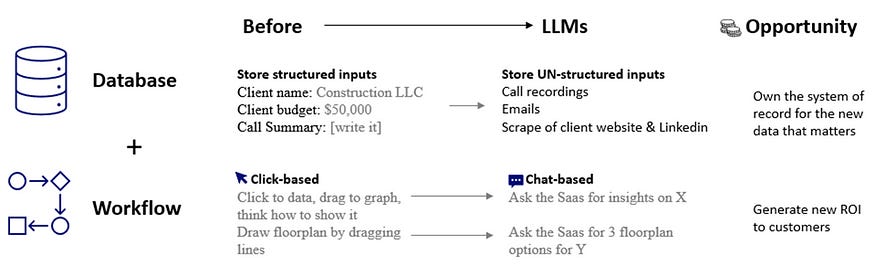

As mentioned, a vertical SaaS business is (1) a database and (2) workflows for a specific industry. Generative AI (LLMs) affects both.

A database is the system of record. Before LLMs, generally, only structured data was stored. For example, client name, deal size, date of close, etc. This is because structured data is easier to organize into useful structured outputs (e.g. $ in pipeline this week). That was the case until now. Generative AI (LLMs) can now enable the easier use of unstructured data, which doesn’t follow a preset data model. The most common example being text or multimedia. The use case here could extend to emails, call transcripts, and various documents. Based on a call transcript, an LLM could ‘analyze’ what was the estimated deal value of a client based on call dialogue, or what is the “deal win” probability. This would have been extremely complex to do before LLMs. In areas like customer conversations, the ability to store this unstructured data can add immense value. This alone can become a foundational data unit around which a new vertical SaaS could become a system of record.

Workflows are how users input data, visualize insights, and create outputs. LLMs can enable automated inputs from unstructured sources, automatically suggest insights, and automate output creation. For example, email orders could be automatically inputted and responded to by the SaaS/LLM; LLMs can automatically suggest insights from data; and finally, instead of writing that follow-up email, an LLM can craft it.

The opportunity LLMs bring is compounded in industry-specific software given they can be trained on industry specific data. Before, the value proposition of vertical saas was “industry-specific” workflows, now it can also be better performing LLMs or better autonomous agent workflows for specific industry tasks.

In some verticals, incumbent saas providers will be able to leverage existing clients and data to build better workflows with LLMs and improve their defensibility, but in other verticals LLMs may provide new companies an angle to build a new saas leader in their industry. We look forward to supporting those daring to build new leaders.