Serial Acquirers

An introduction

Serial acquirers are holding companies that primarily grow through frequent acquisitions of small, profitable businesses. This strategy has given rise to very large companies, including Transdigm ($77Bn), Constellation Software ($70Bn), Copart ($50Bn), Danaher ($200Bn), Lifco ($15Bn), Halma ($13Bn). Early investors in these companies have enjoyed stellar returns, in line with outlier venture investments.

An investment in Constellation Software in 1995 would have yielded a staggering 1,700x return—8x in the first 10 years and 200x in the 20 years since its IPO. Similarly, investing in TransDigm since 1998 would have resulted in approximately 600x in value (~10x in the initial 10 years and 60x in the 20 years post-IPO). Copart has delivered 360x returns since 1994 (10x in the first 10 years). Teledyne returned 233x to early investor Arthur Rock, the venture capitalist who also backed Apple.

Despite their success, serial acquisition businesses are often overlooked by investors. The failures of some M&A roll-ups discriminate too broadly. Additionally, analysts tend to be conservative and overlook the value of a strong team capable of generating a robust M&A pipeline.

How serial acquirers add value

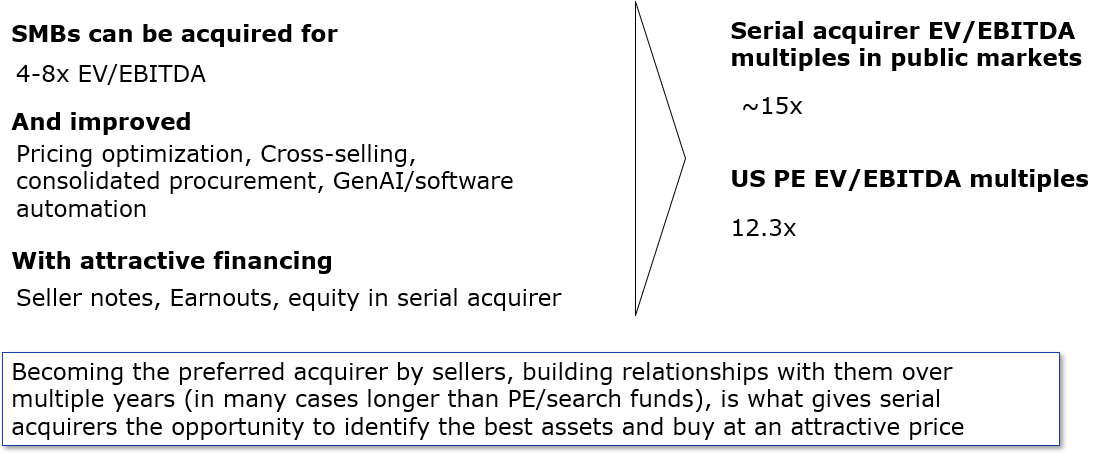

Serial acquirers excel by becoming the preferred buyer in their niche (low entry price, access to best assets) and having a playbook of value creation (price increases, workforce optimization, procurement savings). Excess cash flows are funneled back to HQ to fund further acquisitions, creating a compounding growth effect.

Excess multiples are justified by an M&A team that can continue to redeploy cash flows at attractive ROICs, and because a larger business is more stable.

Common traits between serial acquirers

Acquire programmatically: ~10 acquisitions a year per M&A team at scale

Hold for long periods of time

Asset-light models: “A few serial acquirers didn’t have the ‘asset-light epiphany’ until after they’d struggled with more capital intensive businesses”

Niche focus: niches have high barriers to entry relative to TAM, but low reinvestment opportunities

Frugal HQ sets the pace for the other companies in the holding

Differences between serial acquirers

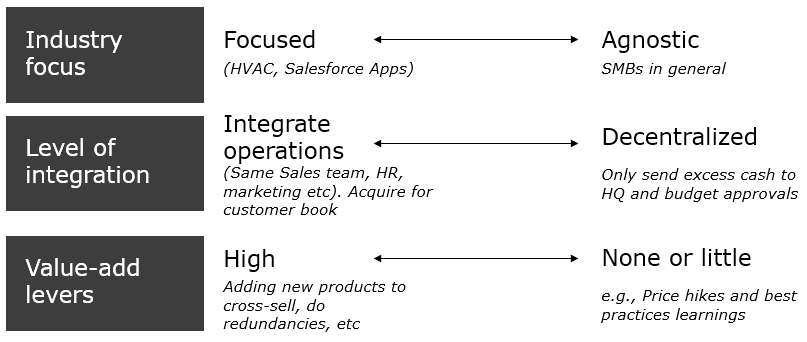

Integration of acquired companies: Some acquirers give operators independence post acquisition, others rollup clients into a consolidated platform.

Industry focus: Some acquirers have a narrow industry focus (e.g. pool maintenance), while others target small businesses in general.

My less obvious learning was that decentralized approaches work well, leaving companies independent post acquisition, only providing learning and incentives and taking excess cashflow back to HQ. Not saying that integrating companies does not work well, but I am saying that depending on the target industry, integrating is not the only way to create value. Decentralization can mean attracting sellers that want to keep their legacy or want to continue operating the business, and in a lot of cases avoiding large HQ costs in the name of synergies. These benefits can outweigh the potential cost savings from consolidating departments and the ‘cross-selling’ opportunities. The optimal choice is very industry-specific.

What makes for a good target industry

High ROIC: actuarially recurring revenue, not capital intense (low additional capex needed to scale and ideally low working capital increases needed to scale). Ideally growing end market. Ideally high cash flow margins

High defensibility / high retention: For example this can be achieved through a local brand, high switching costs (mission critical), a regulatory reason, product development, network effects, a cost advantage through economies of scale

A fragmented industry with a large acquisition pipeline

Unique value levers on acquisition: there may be a latent price increase opportunity (like Transdigm saw in low complexity airplane parts or Constellation saw in vertical software), there may be instant procurement cost decreases (e.g. IT service providers that become gold partners on acquisition), or a unique additional revenue stream added (e.g. Copart acquired junkyards and sold the car parts on its online marketplace)

Good founders not only focused on high quality businesses, but stayed at disciplined buy-in multiples. Constellation Software only has contemplated reducing their 25% ROIC threshold on acquisitions after 25 years in operation and billions a year of capital to redeploy

What makes for a good founder

While there is no hard rule, studying tens of successful serial acquirers (and tens of failures), has taught me the following about successful serial acquisition founders:

Think like capital allocators and operators

They are multidisciplinary rather than subject matter experts. In fact many were not subject matter experts in the industry they were targeting initially

Independent thinkers that didn’t blindly copy peers, were selectively contrarian. They were committed to rationality, to the data, to thinking for themselves

Frugality in HQ spending

Charisma didn't matter

Had a focus on cash flow based KPIs

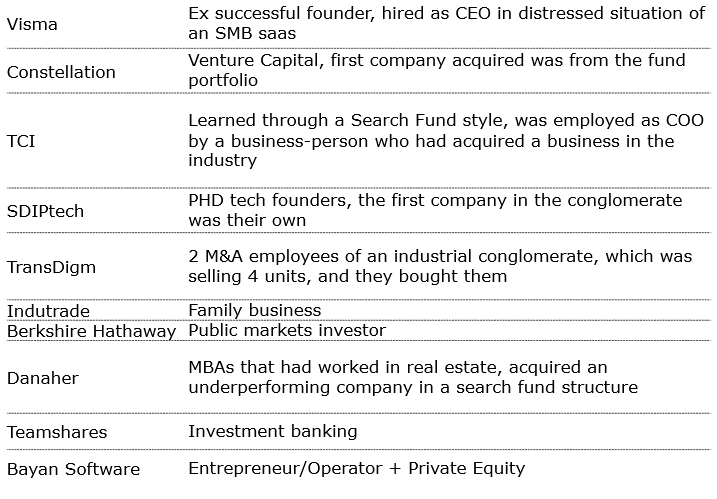

Some backgrounds of successful serial acquirer founders:

Many good serial acquirers were led by a capital allocation leader, but supported by another leader in operations, be it a founder, a hire or from an acquired company. Mark Leonard from Constellation had the founders of some of the early companies play these roles (Mark Miller who is the head of one of the largest Constellation operating units was the CEO of the first acquired company in 1995, Jeff Bender who leads the other large group, Harris, was a company acquired in 1999)

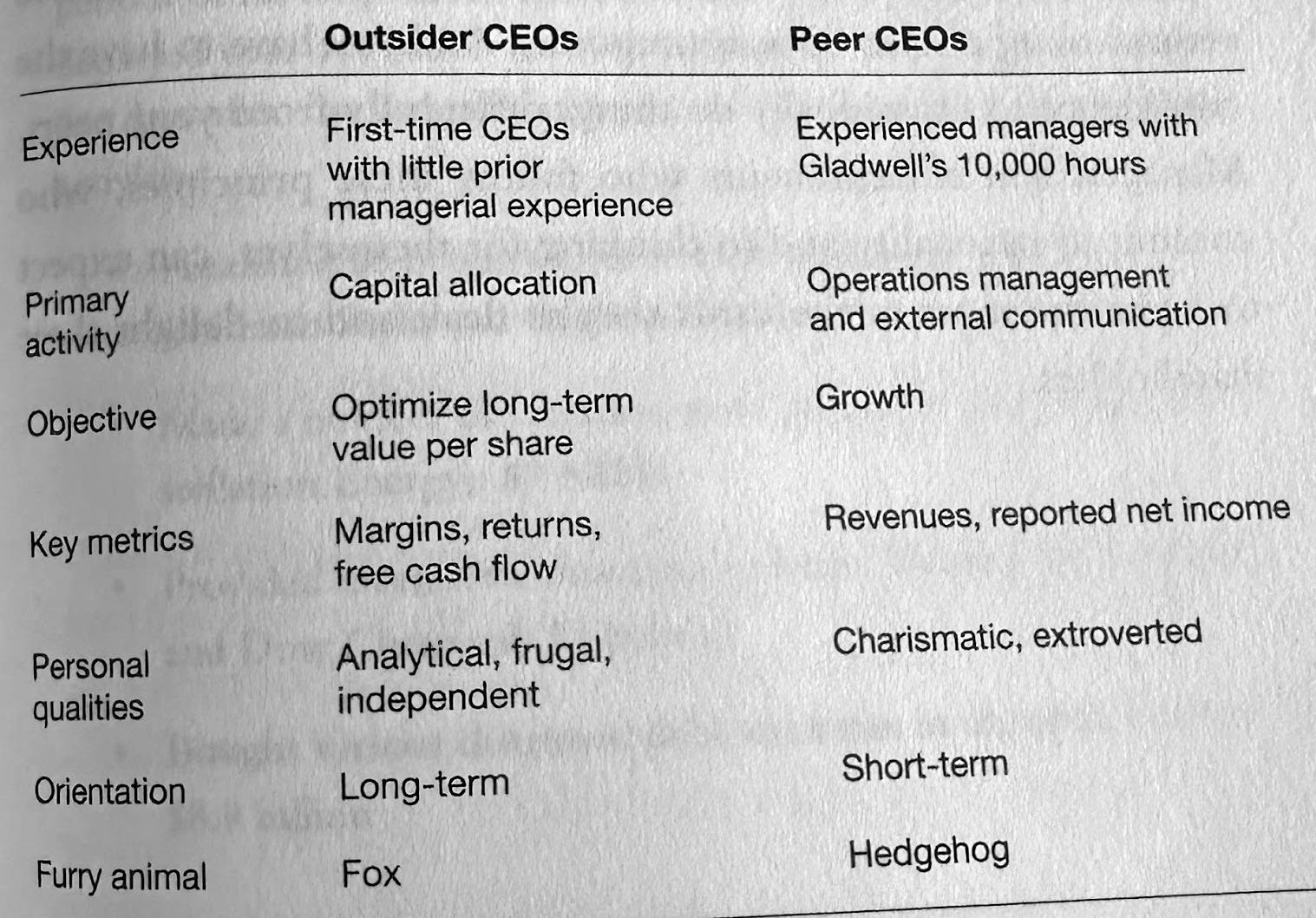

Will Thorndike conducted an analysis of the common trades of CEOs that produced the largest returns vs peers in their tenures. Many were serial acquirers. The characteristics can be a source of inspiration on how to asses serial acquirer CEOs

Why serial acquirers fail

I highlighted the high returns available in this asset class, but there are also numerous failures. Building a serial acquirer is not dissimilar to building a startup, you are still ‘jumping off a plane and building the parachute on the way down’. Common themes of serial acquirer failures included the following characteristics:

Buying a lot in ‘hot’ rollup markets. Going after an ‘hot’ industry lots of others are going after can lead to paying too much for acquisitions

The psychology of the moment is understandable. You just raised a lot of money from investors who expect you to grow through acquisitions at a fast pace. It's hard to sit back, face your investors, and wait for better times or redeploy capital in another industry

Coincidentally, investors will be more willing to back serial acquirers in hot markets

Funeral Homes were hot in the 90s (ending with Loewen), ecommerce sellers were hot in the late 2010s (ending with Thrasio)

Overextension of leverage, specially in low retention businesses. In a turnaround of the market cashflows can reduce, and the company not be able to maintain its debt ratios or pay interest. All serial acquirers are likely to face tough times at some point, and they should allow margin for error.

In 1997 and 1998 a slight death rate decline meant Loewen funeral homes did 3.2% lower sales. They were not able to react by reducing costs and went from $40M profit to $600M loss in a year. They could not meet interest payments and filed for bankruptcy in 1999.

Similarly, Thrasio fell after a deceleration of ecommerce after the Covid-19 faded away.

Pluribus Technologies acquired saas ($75M) around elearning (which started declining in revenue) and in ecommerce (which suffered post covid and went flat). They hit their Debt/EBITDA covenants and the bank may have to restructure

Overestimating cost synergies, both in backoffice and COGS.

Routinely, I’ve heard the story that instead of having thirty HR departments, thirty accounting departments, thirty purchasing departments, thirty marketing departments, the holding company will have one of each. But operations are more nuanced, I saw this while helping with large M&A integrations at Mckinsey, we could generate some synergies locally, but not at scale across the orgs

These lack of efficiencies can be specially acute when existing management is left in place and a decentralized strategy is kept. This is usually done to avoid churn post acquisition

Sometimes serial acquirers can create “Diseconomies of scale”, with additional functions at HQ and reporting needed, or loss of customers due to not being an ‘independent brand’

Overestimating cross-selling, either misjudging customer behavior or misjudging management incentives. In the 1990s, Northwestern Corporation, a provider of electricity and gas, pursued rollups in HVAC and local phone carriers, in the view that because they were the same customers, they would be able to cross-sell. The cross-sell didn't occur at scale. In 2002 they wrote off all of the phone and HVAC investments and in 2003 declared bankruptcy

Overestimating the change that can be imposed on management. Medpartners rolled up small doctor practices in the 90s, thinking that they would get doctors to adopt changes like new software and other business practices. This change didn't happen and Medpartners found themselves in huge losses (-50% Ebitda on 2.6Bn of revenue).

Decentralization or Integration can both be possible paths to a successful serial acquirer, but it’s hard to do both at the same time. Decentralization allows to keep the churn post acquisition lower, but it will not allow many cost or revenue synergies. Integration may allow for certain synergies, but should account for possible initial customer churn and additional HQ costs.

In the earlier stages, I have seen serial acquirer founders regret buying small (<0.5M EBIT or organizations with no middle management). The time dedicated to management was large vs the impact generated, so the time to build the future M&A pipeline was limited.

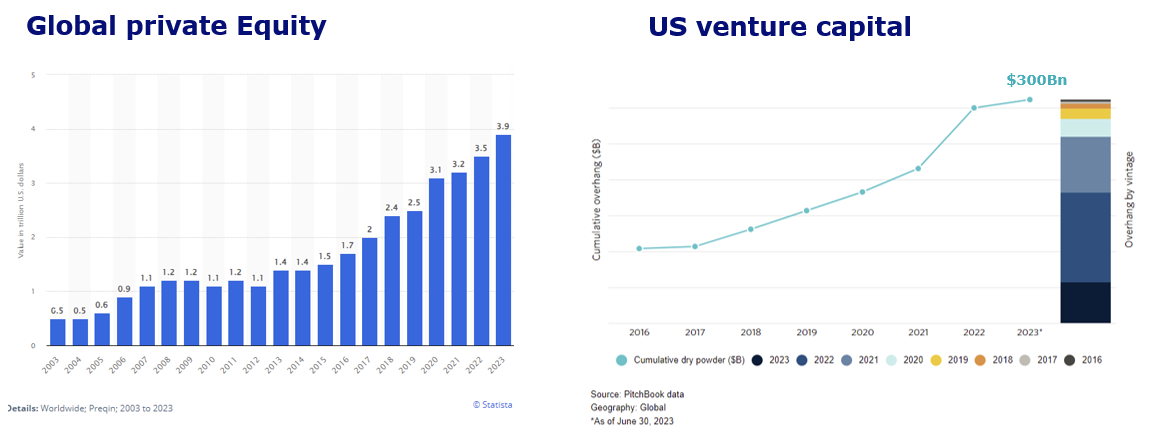

In a time when private market excess returns are harder given the dry powder in PE and VC, serial acquirers may be a niche asset class that produces alpha in private markets

Each of the sections I spoke about could be a book by itself, and there are so many serial acquisition company case studies that could cover a whole chapter. This is only a small general framework.

If you want to talk about serial acquirers don’t hesitate to reach out!

Appendix 1. Dry powder in private markets is growing

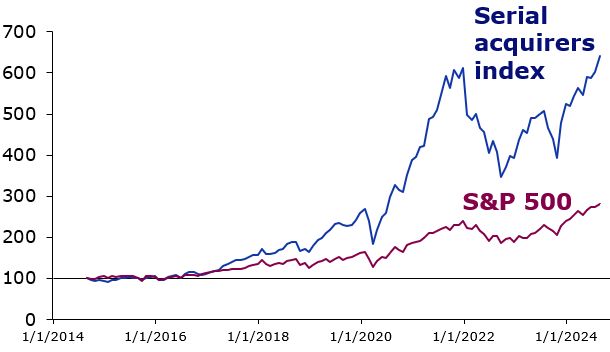

Appendix 2. Public market performance of Serial acquirers index (a custom index with 45 publicly traded serial acquirers, equal weighted) vs S&P500 over the past 10 years